By: Navneet Dubey

The WGC report revealed consumers are becoming more discerning, choosing lighter-weight and lower-carat jewellery

Navneet Dubey is a Senior Associate Editor at Money Today. With over 11 years of experience in business journalism, he specializes in demystifying banking and personal finance, focusing on topics such as retirement planning, investment strategies, and wealth management. His work has been featured in prominent publications including LiveMint, Business Today, and Fortune India.

Preston is the artificial intelligence that powers the Intelligent Relations PR platform. Meet Preston

India (National)

Not enough data

Navneet Dubey's articles predominantly focus on investment analysis and citing data in the areas of personal finance, finance & economy. His coverage indicates a strong interest in providing insights into financial decisions that affect individuals and businesses. To effectively reach out to Navneet, consider offering expert advice or analysis related to investments, taxes, insurance, income tax changes, budget implications for personal finances or economic trends impacting individual financial decision-making.

Given the nature of his articles which often cite specific data points and provide investment analyses related to budgetary announcements and other financial aspects affecting individuals, it would be beneficial to provide well-researched insights supported by credible sources or statistical evidence when reaching out to him.

This information evolves through artificial intelligence and human feedback. Improve this profile .

By: Navneet Dubey

The WGC report revealed consumers are becoming more discerning, choosing lighter-weight and lower-carat jewellery

By: Navneet Dubey

The jump in ETF investments suggests that Indian investors are distinguishing between gold as a consumption product and gold as a financial asset

By: Navneet Dubey

The RBI rolled out this special window that could help strengthen the country's foreign exchange reserves and boost overseas capital inflows

By: Navneet Dubey

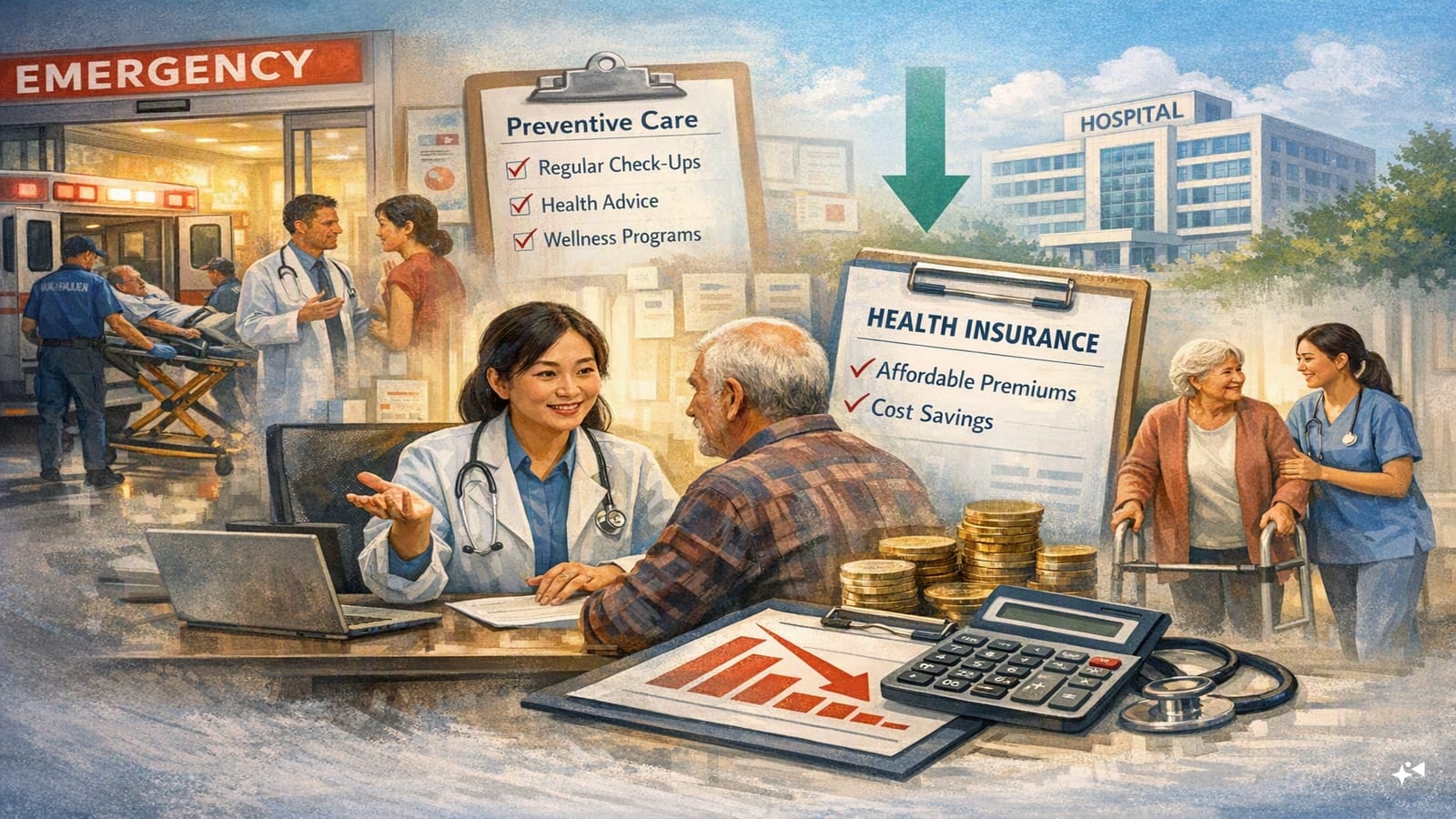

Responding to criticism from sections of the medical fraternity, the GIC emphasised that the advisory is not mandatory and does not override a doctor's clinical judgment

By: Navneet Dubey

Responding to criticism from sections of the medical fraternity, the GIC emphasised that the advisory is not mandatory and does not override a doctor's clinical judgment

By: Navneet Dubey

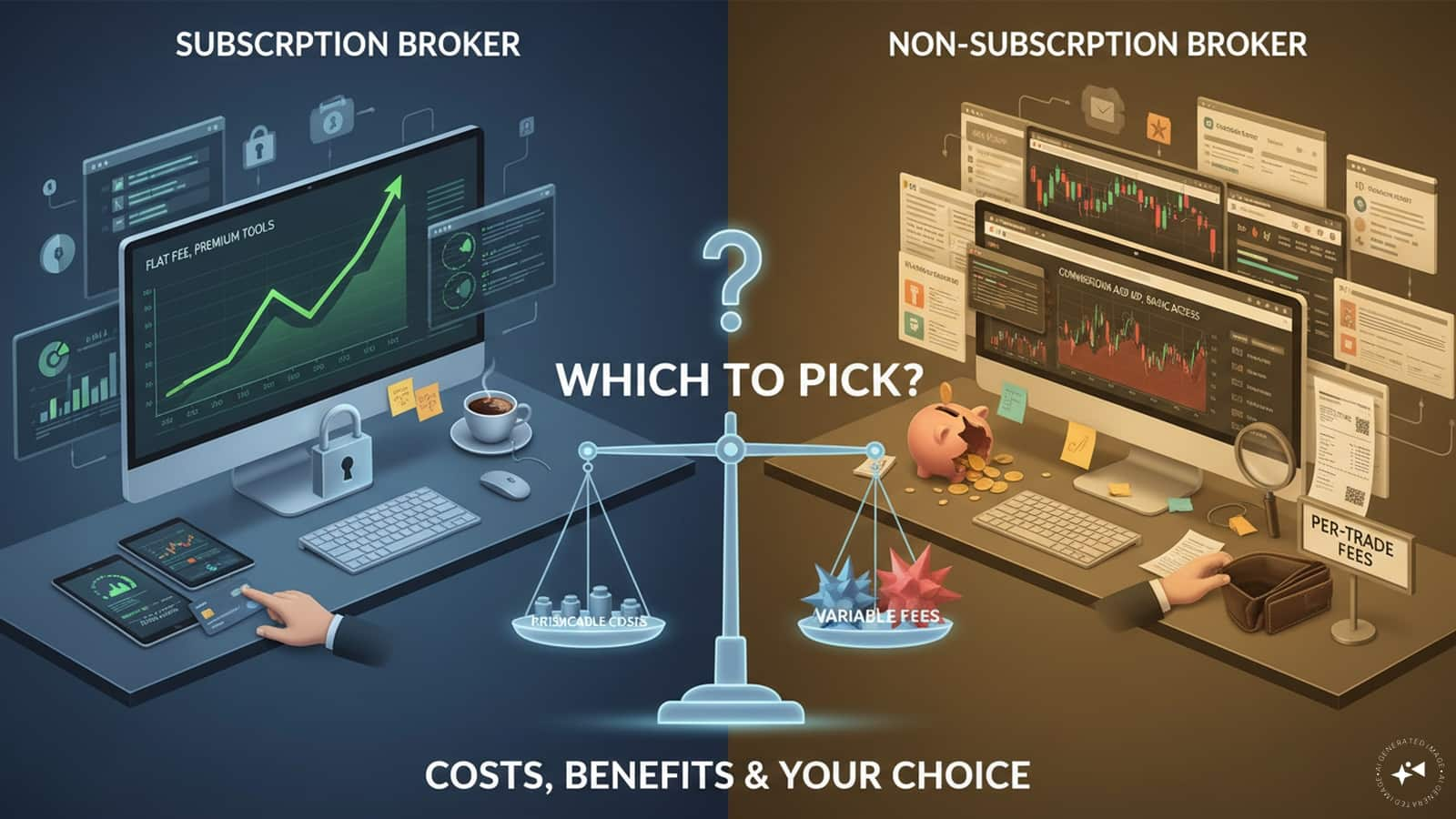

The subscription economy creates a paradox. Each service appears affordable in isolation, but together they can quietly consume a sizeable share of monthly income

By: Navneet Dubey

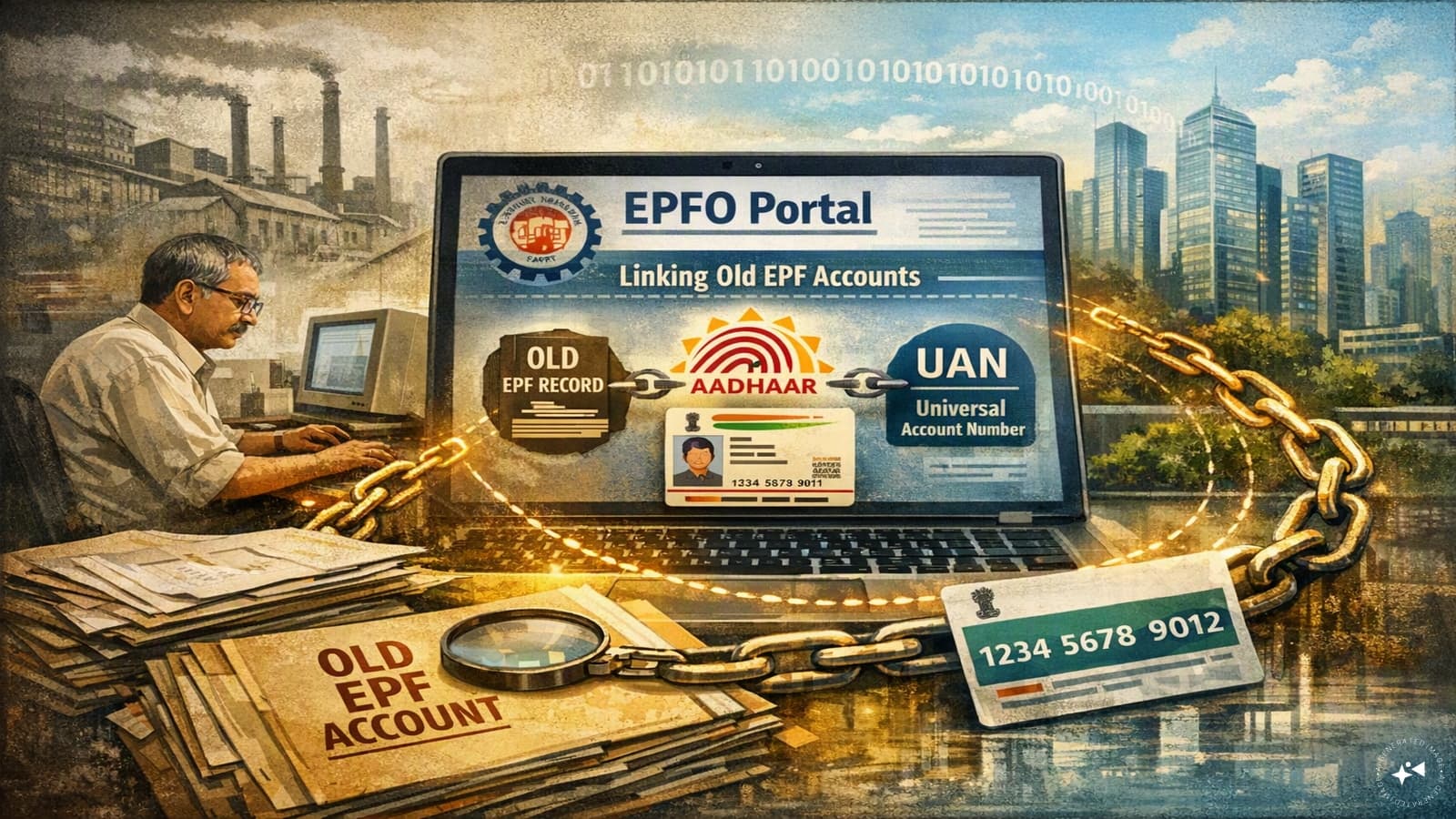

Employees who do not know their earlier UAN should first approach their previous employer, who can retrieve it through the EPFO employer portal

By: Navneet Dubey

SBI has emerged as the largest mobiliser of FCNR(B) deposits under the RBI's swap window

By: Navneet Dubey

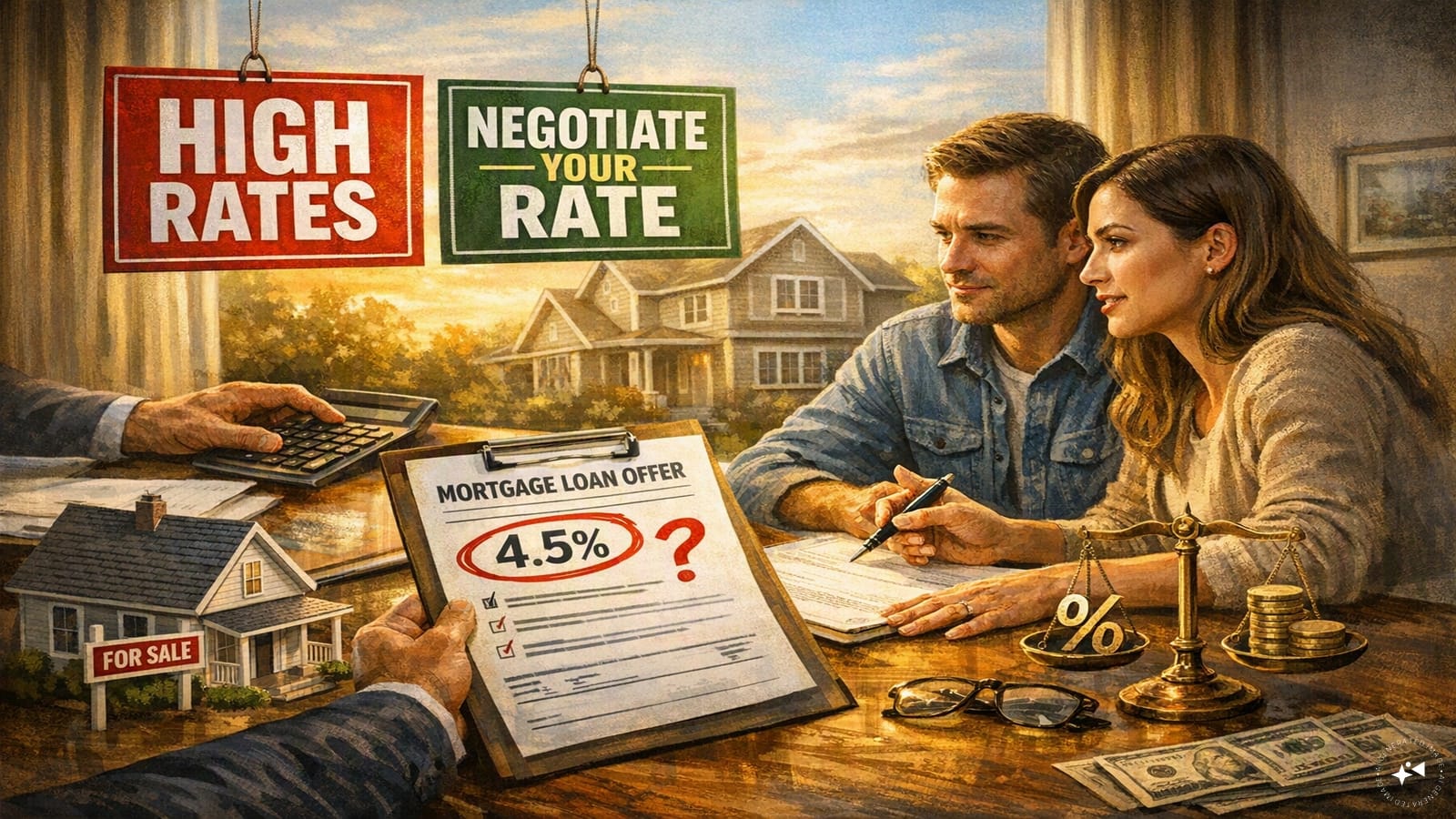

Lenders sometimes revise rates for existing borrowers

By: Navneet Dubey

Many newer subscription plans attempt to bring these services together within a single ecosystem, reducing the need for traders to rely on multiple third-party platforms